Should 695 reward volunteers?

Everyone has limited availability and resources, with wide variations in priorities, interests and family obligations. AFSCME Local 695 appreciates if volunteer members are able to make sacrifices, but fully understands members living paycheck-to-paycheck simply may not have any extra out-of-pocket cash, or time, to be lost.

Doing Local business is what lost time is for. A second paycheck can result by running for Local office or by serving as delegates, guests or alternates to perform constitutional or contractual roles at Local, Council and International functions, events, meetings, conventions, plenaries, committees, and labor affiliations. COVID re-defined the way members attend these events. Some examples:

Biennial AFSCME Statewide Agreement negotiations assemblies

Council 5 Spring/Fall conventions

Policy Committees (both entire state and more granular by department or agency)

District Safety and Equipment Committees

District and Statewide Labor/Management Meetings

Affiliate meetings (AFL/CIO-MN, Duluth Central Labor Body)

National/International events

What are labor's interests, the interests of working people, and how best to protect them? COVID increased the number of workers experiencing economic stress and surviving on assistance, and this global pandemic unleashed additional uncertainties such that more than a few workers see fearful doubts clouding their futures.

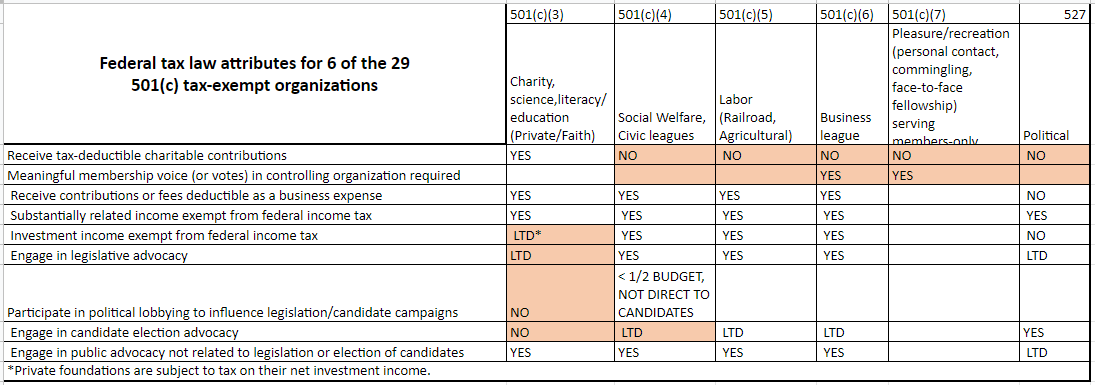

Labor unions are IRS code 501(c)(5)s tax exempt, while nonprofits formed for religious, charitable, scientific, literary, or educational purposes are IRS code 501(c)(3).

IRS non-profit metaverse

Tax code laws limit, discipline and very tightly control what unions can legally, openly do financially. According to Council 5's 501(c)(5)s tax exempt filing for 2019, "AFSCME Council 5 is a union of 36,000 members who advocate for excellence in services for the public, dignity in the workplace, and opportunity and prosperity for all working families."

The IRS allows labor unions to recompense travel-related expenses, when doing union business, and in some cases lost time, especially when there is above-and-beyond work substantially related to a core labor union mission, such as lobbying and negotiating for better employee wages and benefits. AFSCME Council 5's mission further defines this by implying a constitutional right of free speech must be prerequisite to conduct labor union advocacy to lobby and negotiate for better wages and benefits.

Unions can party, can even throw very big parties, banquets where working parents are welcome to bring their children and meet personally, face-to-face, off the clock and completely outside of work’s constraining rules and rigid formal policies. Local 695 does this by sponsoring annual dinners and picnics, but no one mistakes by having fun together, 695 is not being a union, or is trying to be more like a professional or employer-controlled social association, where one would never hear rabble rousing plots to get better wages and benefits.

Membership meeting motions to respect traditional holiday seasons, or specific sectarian or cultural observances, by giving out rewards, are expressing a mood to give. Can the Local offer one person tangible recognition for their personal accomplishment, embarrass some volunteer avoiding recognition by giving cash? Whether motivated by season's tidings, or by a shared feeling to express gratitude, esteem or favor, in doing these giving things unions must carefully avoid "inuring excess benefits" because that can cross IRS lines. State policy on gifts, gift cards, allow that when co-workers financially recognize an individual by offering a tribute to someone for major life events, such as births or weddings, these occasions are infrequent enough that acceptance does not raise either ethical or IRS flags.

Unions must be able to prove expenditures, including rewards and season-appropriate gifts, legally fit their tax-exempt mission on file, with records retained of that proof, or risk being stripped of tax-exempt status. Hard-copy records proving this are usually checks, and when these are lost, thrown away or held uncashed, tedious notifications and costly follow-through with banks are necessary to arrange paying cancellation fees. Canceled checks are about the most easily audited kind of legal tax record.

AFSCME Local 695 issues checks which require two officer signatures (held on file at the bank for that account) and 695's constitution states the two offices with authority to sign Local checks must face reelection with a one year offset, one elected odd years, the other even years. Hard copy printed checks have human-readable magnetic ink account numbers, and are not secure but are used by 695 to avoid impossible-to-document cash, virtual currency or cards lacking recurring statements.

{kind=link}

Members in elected office, or claiming lost time, or those serving in positions that pay allowances, must file tax form W-4 at the Council's MemberLink. Entries in 695’s expense voucher lower area are how LUP (Local Union Payroll) is enabled for Council 5 to direct deposit some of the 60% of dues (non-negotiable tax collected by the Council) into member bank accounts. C5 LUP deposits for the Local can go to a different bank account than an employee uses to receive State of MN employee payroll deposits. On the flip side of vouchers, 695 lists the most recently updated common Local business expense amounts, such as lost time days and travel-status meals, plus clues where to find further details.

Estimated expense advances are available for volunteers anticipating travel. Vouchers for usual and customary expenses (IRS-speak for travel-related meals, lodging, parking and mileage) are due within 30 days to 695’s Treasurer. In reimbursing mileage expenses to attend meetings, the IRS allows labor unions the current full federal standard mileage rate used by the State of MN, which is nearly five fold higher than volunteer drivers can claim for driving patients to medical appointments.